In recent years, Andorra has become an increasingly attractive tax destination, which is why more and more individuals and entrepreneurs are seeking to become residents in Andorra.

This small principality offers a favorable tax system, with a maximum personal income tax (IRPF) of 10% and a corporate tax rate of 10%, making it one of the most competitive options in Europe. In addition, Andorra does not impose wealth or inheritance taxes, making it an ideal place for those looking to optimize their income and protect their assets.

Furthermore, the range of profiles interested in tax residency in Andorra is becoming increasingly diverse. From business owners and entrepreneurs seeking to establish their companies in a tax-friendly environment, to freelancers, investors, or retirees who wish to benefit from its low tax burden and improve their quality of life.

Andorra also attracts families and elite athletes, who value its safety, high-quality healthcare services, and natural surroundings. As such, Andorra presents itself as a strategic option for those looking to improve both their financial and personal situation.

What is tax residency?

Tax residency is the legal status that determines in which country a person or company is required to pay taxes on their income and assets. It is defined based on factors such as the number of days spent in a country, the location of the center of economic interests, or the individual’s habitual residence.

Being a tax resident in a country means complying with its tax obligations, including reporting and paying taxes.

Tax residency status may change if the requirements of another country are met, which can lead to potential tax benefits or advantages.

What types of residence permits are available in Andorra?

Before going into detail about the requirements for obtaining tax residency in Andorra, it is important to distinguish between two concepts that are often confused: administrative residency and tax residency.

Administrative residency is granted by the competent immigration authorities. Tax residency, on the other hand, is not acquired automatically at the same time, but is established once a series of requirements set out in current tax legislation have been fulfilled.

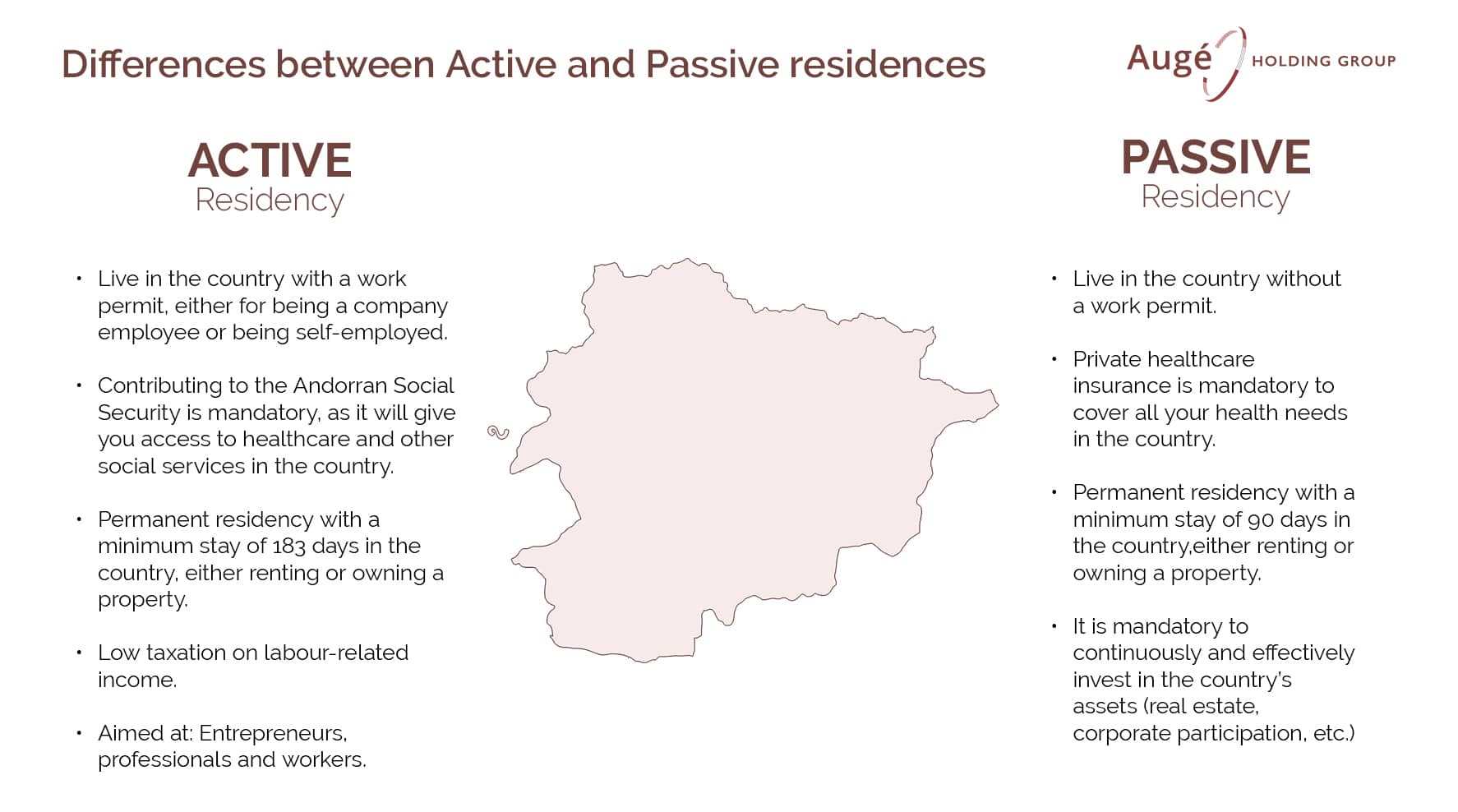

There are different ways to obtain administrative residency, which can be broadly divided into active residency and passive residency.

Active residency

Active residency includes employees and self-employed individuals or entrepreneurs.

Employment residency (or salaried work) is obtained through an employment contract. This type of residency requires living in Andorra and carrying out work physically within the country.

There is also self-employed residency, which requires carrying out an economic activity through the creation of a company in Andorra. In this case, a minimum presence of 183 days over the course of a calendar year is required, along with a mandatory non-refundable deposit of €50,000, fully owned by the state and not reimbursable to the applicant. This measure is established under the so-called “Omnibus Law 2,” approved by the Consell General and published in the official gazette (BOPA) on February 12.

This model is similar to the concept of being self-employed in Spain. It is important to note that the applicant must act as a company director, hold more than 34% of the company’s shares, and contribute to the Andorran social security system. In short, this is the primary model for running a business in Andorra.

Passive residency

Passive residency applies to retirees, individuals with passive income, or investors. It is also known as non-lucrative residency and requires an investment in debt or financial instruments issued by resident entities or in Andorran collective investment funds, with a maximum duration of 36 months. After that period, the investment must be redirected into other qualifying assets in order to continue being valid. The minimum investment in Andorran assets must be at least €1,000,000.

Additionally, a mandatory deposit of €50,000 is required for the main applicant, plus €12,000 for each dependent. These amounts are considered final, non-refundable contributions (except in case of initial rejection).

For this type of residency, the only requirement is to reside in Andorra for at least 90 days per year. In general, since passive residency does not allow for economic activity, it is typically intended for individuals who are already retired and wish to manage their wealth from Andorra, thereby benefiting partially or fully from the advantages of being a resident in the principality.

Discover how to move your residence to Andorra: requirements, tax benefits, cost of living and new opportunities in the country of the Pyrenees.

Read MoreRequirements to change tax residency to Andorra

The criteria for considering a person a tax resident in Andorra are governed by the general rules of the OECD, adopted in the Principality and duly set out in Andorra’s personal income tax (IRPF) law.

Among the requirements, you must meet certain eligibility criteria and gather the necessary documentation for the process.

Eligibility criteria

The law establishes that a person will be considered a tax resident in Andorra if they meet the following conditions:

- You reside in the country for more than 183 days per year, taking into account that days spent traveling abroad are also included.

- Your center of economic interests is located in Andorra, meaning that your main source of income comes from the Principality.

- Your family or vital interests (in the case of being married) are based in Andorra, or you have dependents residing in the country.

Required documentation

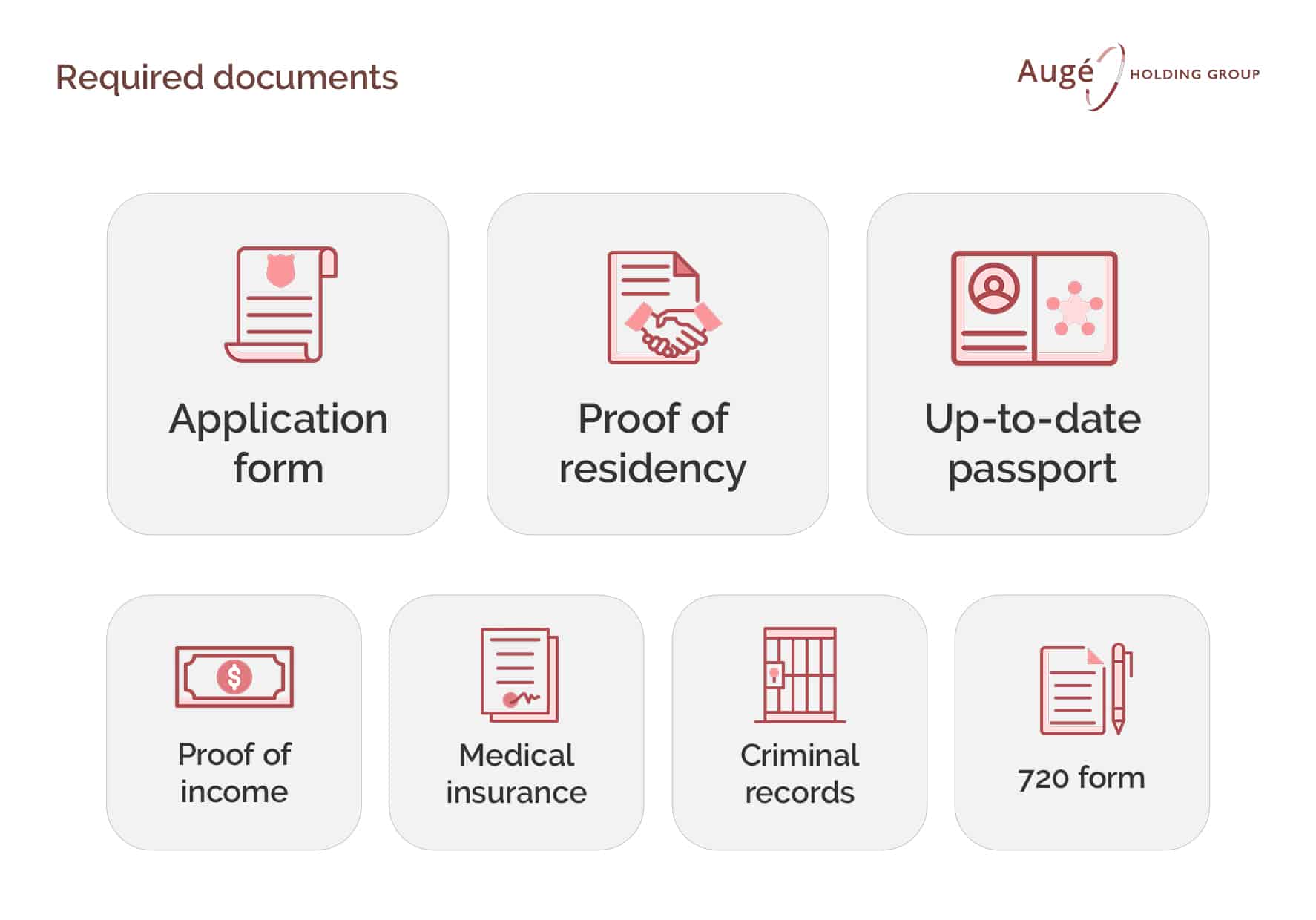

There are eight different categories of information that you must gather before applying for residency in Andorra.

- Tax residency application form, submitted to Andorra’s Immigration Department.

- Proof of residence in Andorra, such as a rental agreement or property deed. This document must demonstrate that you reside in Andorra for more than 183 days per year.

- Valid passport, with a minimum validity of six months from the date of entry into Andorra.

- Proof of income, to demonstrate that you have sufficient financial means to live in the country. This may include:

- Bank statements from accounts in Andorra or abroad

- Income documentation such as salary slips, rental income, or any other source of earnings. If you own a business, you must also provide profit certificates or an income declaration

- In some cases, a minimum balance in an Andorran bank account may be required to prove financial stability

- Health insurance, either private or public, if you are registered with the Andorran Social Security system (CASS)

- Criminal record certificate from your country of origin and from Andorra. This document must be legalized with the Hague Apostille and issued within the last three months

- Form 720, used to declare assets held abroad, which must be submitted to the Andorran tax authorities. As a tax resident, you may need to report your foreign assets

- Certificate of non-tax residency from your country of origin (in many cases), to prove that you are no longer considered a tax resident there

What is the administrative process to apply for tax residency?

Applying for tax residency in Andorra involves several steps, from gathering documentation to submitting the application to the authorities. Below is a step-by-step overview of the process.

How to submit the application

Once you have gathered all the required documents, you must submit your application to the Immigration Department of the Government of Andorra, which is responsible for processing all residency applications. You can do this in two ways:

- Online application: through the official government portal (in some cases, you may still be required to appear in person to complete certain procedures)

- In-person application: at the immigration offices in Andorra la Vella, where you will submit all the documentation along with the completed application form

Estimated processing times

The time required to obtain residency in Andorra may vary depending on the type of residency and your specific circumstances, such as the amount of documentation required or whether additional proof is needed. However, in general, the evaluation process takes between 4 and 6 weeks. Estimated timelines by residency type:

- Active tax residency (employees and entrepreneurs): 2–4 months

- Passive residency (investors and retirees): 3–6 months

- Residency by investment (golden visa): 2–3 months

- Entrepreneur residency (SMEs and startups): 3–5 months

What is the minimum stay requirement?

The minimum stay required to be considered a tax resident in Andorra is 183 days per year. This is the key criterion that determines your tax residency status, regardless of whether you reside full-time or part-time.

Individuals with active residency must meet the 183-day requirement and be registered with the Andorran Social Security system (CASS).

Individuals with passive residency, even if they are not working in Andorra, must also maintain a physical presence in the country for at least 183 days per year.

What are the tax advantages of residing in Andorra?

Being a resident in Andorra gives you tax advantages that you would not have in in many European countries because taxes in Andorra are considerably lower. This makes the Andorran principality a very attractive tax destination. With a maximum personal income tax rate of 10%, a corporate tax rate of 10% and the absence of wealth and inheritance taxes, residing in Andorra allows for significant tax optimization. These advantages, together with the high quality of life, make Andorra an ideal choice for entrepreneurs and investors.

Income Taxe

Income taxes in Andorra are at a very low rate. Personal income tax is considerably lower than in many other countries. The maximum rate is 10% on personal income, one of the lowest figures in Europe.

In addition, although the tax rate is low, Andorra’s personal income tax system is progressive, being applied as follows:

- Up to €24,000: 0%.

- Between 24.000 € and 40.000 €: 5%.

- From €40,000 and above: 10%.

This system benefits those with moderate or high incomes, since the tax rate does not exceed 10%.

Wealth and Inheritance Tax

There is no wealth tax in Andorra, which means that you are not directly taxed on the value of your personal assets, such as real estate, financial investments or any other assets.

As for inheritance and gift tax, Andorra also has advantages, as it does not apply a significant tax in these cases, which facilitates the transfer of assets to heirs.

Benefits for investors and entrepreneurs

Andorra offers tax advantages for entrepreneurs wishing to establish a company or startup in the country. Investors or entrepreneurs residing in Andorra can benefit from a 10% corporate tax rate and relatively low costs when starting a business. This makes Andorra a very competitive place to set up and run businesses.

In addition, there are government incentives that encourage foreign investment, such as tax exemptions and facilities for the creation of new companies in sectors such as tourism, technology and finance.

If you are a resident of Andorra and have investments abroad, such as shares or investment funds, you are generally not required to pay taxes on those assets in Andorra, as there is no wealth tax or double taxation on international investments.

Moreover, Andorra has agreements with certain countries to avoid double taxation, which facilitates the tax optimisation of investments in other countries.

Cost of living in Andorra vs. EU

Generally speaking, Andorra tends to be an attractive destination for its tax benefits and quality of life, although some aspects of the cost of living can be higher than in other areas throughout Europe.

This is largely due to the cost of housing, a scarce commodity in Andorra, given its small land area, compared to other countries in Europe. In January 2024, the average purchase price per square meter reached 4,582 euros, according to data from Idealista.

On the other hand, the cost of the shopping basket may be slightly higher than in surrounding countries, although the differences are not very significant. However, typically expensive products, such as tobacco or alcohol, are much cheaper, mainly due to the absence of taxes on their price.

Gasoline deserves a whole other chapter, which is still much cheaper than in other countries, despite the escalation of prices linked the rise of crude oil. This also impacts transportation, making it significantly cheaper than in Spain and other countries in the region. Additionally, purchasing and maintaining your own vehicle is also cheaper than in the rest of the Peninsula.

In short, although certain aspects of the cost of living in Andorra make it a more expensive option than other countries in Europe, the tax advantages enjoyed by the principality compensate for this difference and make it a more than recommendable destination to reside.

Following the end of the UK non-dom regime, Andorra is emerging as a safe, transparent, and competitive tax destination for international wealth management.

Read MoreCan I have tax residence in Andorra and live in my country?

Yes, it is possible to have tax residency in Andorra and live in another country, but this scenario involves certain tax risks and legal conditions that you must take into account to avoid problems with your country’s Tax Agency.

You can be considered a tax resident in Andorra if you meet the residency requirements, which include living more than 183 days a year in the country or having the effective address of your economic activity in Andorra, i.e., having your centre of economic and personal interests in Andorra.

The main risk of living abroad and having your tax residence in Andorra is that your country’s tax authorities could consider that you are actually a tax resident there.

This would happen if they prove that your centre of economic and family interests is in your country, which would contradict your tax status in Andorra. If that happens, you should comply with your country’s tax obligations, which implies paying taxes on your worldwide income, no matter where you generate it.

To minimize risks, make sure you have clear proof of your residence in Andorra such as documents or contracts, and of the place where your economic and family interests are actually developed. Otherwise, you could face problems with double taxation and fiscal obligations in both countries.

The same applies to any other nearby country in which you wish to live while maintaining tax residence in Andorra.